How to Calculate and Forecast Purchase Price Variance (PPV)

PPV can be used in budgeting, performance measurement, financial planning, and forecasting. Learn the main calculations and data you will need.

Tell Me MoreUpdated: Mar 9, 2026

In any manufacturing company, Purchase Price Variance (PPV) Forecasting is an essential tool for understanding how price changes in purchased materials affect future Cost of Goods Sold and Gross Margin.

This helps business stakeholders make more informed pricing decisions and finance functions provide more accurate forward-looking statements on overall future profitability.

In this article, we'll explain what PPV is, how it's used in budgeting and performance measurement, and how to forecast it.

How to calculate PPV

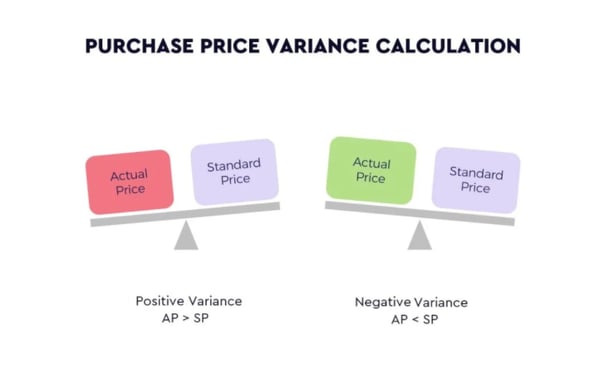

Purchase Price Variance is the difference between the Actual Price paid to buy an item and the Standard Price, multiplied by the Actual Quantity of units purchased. Here is the formula:

PPV = (Actual Price – Standard Price) x Actual Quantity

What Does a Positive or Negative PPV Mean?

- A Positive PPV means actual costs were higher than budgeted — an unfavorable outcome.

- A Negative PPV means actual costs were lower than budgeted — a favorable outcome, typically considered savings.

PPV can be used to quantify the efficiency of a company's procurement function.

Negative PPV is considered savings and thus good performance. However, this is a simplistic view — commodity price volatility is often outside the control of buyers.

In the worst cases, using PPV as a performance measure can drive politics around Standard Price setting rather than motivating genuine procurement improvement.

Interested in diving into more procurement insights? Check out our guide Spend Analysis 101

Why Does PPV Matter in Manufacturing?

PPV matters because direct material purchases can account for up to 70% of all costs in manufacturing companies. Budgeting and tracking material prices is therefore a core responsibility of any manufacturing finance function.

When a financial budget is created, the exact price of materials is unknown, so a best-estimate Standard Price is used. After costs are realized, the Actual Price and Actual Quantity are known, and PPV quantifies the gap between plan and reality.

PPV explains how material price changes have affected gross margin compared to budget. It is a key component in understanding overall business profitability and is typically a standard output of finance ERP systems, where PPV calculations happen automatically.

How Is PPV Used in Financial Budgeting?

In financial budgeting, PPV serves as the bridge between planned material costs and actual outcomes.

When a budget is set, the Standard Price represents the best available estimate of future purchase prices. Once the period closes, finance teams compare the Standard Price to the Actual Price across all purchased quantities to determine whether material costs came in above or below plan.

This variance is then used to explain gross margin movements in management reporting, board presentations, and financial forecasting updates.

What Is Forecasted PPV — and Why Is It Powerful?

PPV is a historical indicator telling you what has happened in the past. Imagine, however, how powerful a forward-looking PPV indicator would be.

Forecasted PPV is a forward-looking version of PPV that estimates how future material price changes will affect gross margin before they happen.

The math needed to calculate Forecasted PPV is straightforward and similar to the Realized PPV formula:

Forecasted PPV = (Forecasted Price – Standard Price) x Forecasted Quantity

With Forecasted PPV, business units gain advanced visibility into how expected material price changes will erode or improve gross margins. This allows teams to:

- Proactively take actions to protect margins

- Adjust sales pricing decisions before cost increases hit

- Give finance teams the data needed for accurate forward-looking profitability statements

What Are the Challenges of Forecasting PPV?

The core challenge is that forecasted PPV cannot be automatically calculated by ERP or finance systems like SAP. Standard Prices are available in these systems, but Forecasted Prices and Forecasted Quantities must be compiled from multiple external sources.

Forecasted Quantity data typically comes from:

- Demand planning and MRP systems

- Extrapolated historical quantities and previous forecasts

- Manual entry and adjustment by people closest to market demand

Forecasted Price data typically comes from:

- Purchasing systems with visibility into contracted prices

- Procurement team estimates based on supply market knowledge

- Cost structure models for key materials

In large enterprises — with multiple source systems, tens of thousands of material numbers, and multiple plants and business units — building and maintaining a regular PPV forecast is a significant operational undertaking.

How Does PPV Affect Gross Margin?

PPV directly impacts gross margin because material costs flow into Cost of Goods Sold (COGS). When Actual Prices exceed Standard Prices (positive PPV), COGS exceeds budget, compressing gross margin. When Actual Prices fall below Standard Prices (negative PPV), COGS is lower, expanding gross margin.

For manufacturing companies where materials account for the majority of product cost, even small per-unit price variances across large volumes can produce significant swings in gross margin. This is why finance teams track PPV monthly and use it as a key line-item explanation in margin bridge analyses.

The data you need

Quantity forecasts are usually the result of combining

- Data from demand planning and MRP systems

- Extrapolated historical quantities and previous forecasts

- Manual entry and adjustment by persons who best understand demand

Forecasted prices can come from purchasing systems with sufficient visibility into contracted prices. Still, procurement people need to manually estimate at least the key materials based on their view of the supply market and using cost-structure models.

In a large enterprise with multiple source systems for forecast data, tens of thousands of material numbers to be forecasted, and a score of plants and business units involved in the process.

Building and maintaining a regular Purchase Price Variance Forecast is not a task to be taken lightly!

What is a good PPV?

Negative PPV (actual price below standard price) is generally favorable and indicates procurement savings. However, context matters — if Standard Prices were set unrealistically low, negative PPV may not reflect genuine performance.

Who is responsible for PPV in a company?

PPV sits at the intersection of procurement and finance. Procurement teams are typically accountable for the price performance, while finance teams measure, report, and forecast it as part of the management reporting cycle.

Why can't ERP systems forecast PPV?

ERP systems like SAP store Standard Prices and record Actual Prices at time of purchase. They have no built-in mechanism to generate forward-looking price estimates — that requires external market data, procurement intelligence, and demand forecasts that live outside the ERP.

PPV Forecasting made easy

Sievo’s Materials Forecasting is a purpose-built solution for all purchase-related forecasting needs. And if you are looking for a system for Purchase Price Variance Forecasting, we got you covered.

But don’t take our word for it. Hear what Chris from Becton Dickinson has to say about Sievo Materials Forecasting:

Intrigued? Request a personalized demonstration from our website.

Everything you need to know about procurement savings here!

This guide explains the 5 major approaches to cost savings in procurement. 23 different savings methods are explained, from Hard Savings to Cost Avoidance. In addition, you'll learn how best to identify, measure, and communicate those savings to your organization.

Related Articles